Contemporary politics,local and international current affairs, science, music and extracts from the Queensland Newspaper "THE WORKER" documenting the proud history of the Labour Movement.

MAHATMA GANDHI ~ Truth never damages a cause that is just.

Sunday, 5 March 2017

Crash course: what the Great Depression reveals about our future

It was the biggest setback to the global economy since the dawn of

the modern industrial age. But did the world’s reaction worsen the

effects of the 1929 Crash? And have we learned from those mistakes?

by Larry Elliott

As the summer of 1929 drew to a close, the celebrated Yale university economist Irving Fisher

took to the pages of the New York Times to opine about Wall Street.

Share prices had been rising all year; investors had been speculating

with borrowed money on the assumption that the good times would

continue. It was the bull market of all time, and those taking a punt

wanted reassurance that their money was safe.

Fisher provided it for them, predicting confidently: “Stock markets

have reached what looks like a permanently high plateau.” On that day,

the Wall Street Crash of October 1929 was less than two months away. It was the worst share tip in history. Nothing else comes close.

The crisis broke on Thursday 24 October, when the market dropped by

11%. Black Thursday was followed by a 13% fall on Black Monday and a

further 12% tumble on Black Tuesday. By early November, Fisher was

ruined and the stock market was in a downward spiral that would only

bottom out in June 1932, at which point companies quoted on the New York

stock exchange had lost 90% of their value and the world had changed

utterly.

A crowd of speculators gather in front of the New York

stock exchange on Black Thursday, 24 October 1929. Photograph:

Keystone-France/Gamma-Keystone via Getty Images

The Great Crash was followed by the Great Depression,

the biggest setback to the global economy since the dawn of the modern

industrial age in the middle of the 18th century. Within three years of

Fisher’s ill-judged prediction, a quarter of America’s working

population was unemployed and desperate. As the economist JK Galbraith

put it: “Some people were hungry in 1930 and 1931 and 1932. Others were tortured by the fear that they might go hungry.”

Banks that weren’t failing were foreclosing on debtors. There was no welfare state to cushion the fall for those such as John Steinbeck’s Okies

– farmers caught between rising debts and crashing commodity prices.

One estimate suggests 34 million Americans had no income at all. By

mid-1932, the do-nothing approach of Herbert Hoover was discredited and

the Democrat Franklin Roosevelt was on course to become US president.

Across the Atlantic, Germany was suffering its second economic

calamity in less than a decade. In 1923, the vindictive peace terms

imposed by the Treaty of Versailles had helped to create the conditions

for hyperinflation, when one dollar could be exchanged for 4.2 trillion

marks, people carted wheelbarrows full of useless notes through the

streets, and cigarettes were used as money. In 1932, a savage austerity

programme left 6 million unemployed. Germany suffered as the pound fell

and rival British exports became cheaper. More than 40% of Germany’s

industrial workers were idle and Nazi brownshirts were fighting

communists for control of the streets. By 1932, the austerity policies

of the German chancellor Heinrich Brüning were discredited and Adolf Hitler was on course to replace him.

Timeline of turmoil

It would be wrong to think nobody saw the crisis coming. Fisher’s

prediction may well have been a riposte to a quite different (and

remarkably accurate) prediction made by the investment adviser Roger

Babson in early September 1929. Babson told the US National Business Conference

that a crash was coming and that it would be a bad one. “Factories will

shut down,” Babson predicted, “men will be thrown out of work.”

Anticipating how the slump would feed on itself, he warned: “The vicious

cycle will get in and the result will be a serious business

depression.”

Cassandras are ignored until it is too late. And Babson, who had

form as a pessimist, was duly ignored. The Dr Doom of the 2008 crisis,

New York University’s Nouriel Roubini, suffered the same fate.

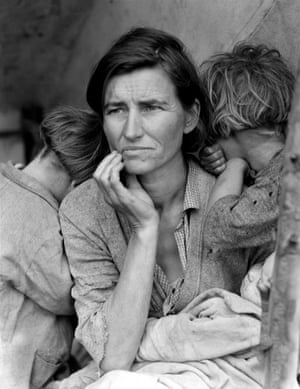

Migrant Mother, 1936, by Dorothea Lange. Photograph: GraphicaArtis/Getty Images

F Scott Fitzgerald described the Great Crash as the moment the jazz age dived to its death.

It marked the passing of a first age of globalisation that had

flourished in the decades before the first world war with free movements

of capital, freedom and – to a lesser extent – goods. In the decade or

so after the guns fell silent in 1918, policymakers had been trying to

re-create what they saw as a golden period of liberalism. The Great

Depression put paid to those plans, ushering in, instead, an era of

isolationism, protectionism, aggressive nationalism and totalitarianism.

There was no meaningful recovery until nations took up arms again in

1939.

In Britain, recovery was concentrated in the south of England and too

weak to dent ingrained unemployment in the old industrial areas. The Jarrow march

for jobs took place in 1936, seven years after the start of the crisis.

It was a similar story in the US, where a recovery during Roosevelt’s

first presidential term ended in a second mini-slump in 1937. Sir

Winston Churchill, who lost a packet in the Crash, described the period

1914 to 1945 as the second 30 years’ war.

Only

one other financial meltdown can compare to the Wall Street Crash for

the length of its impact: the one that hit a climax with the bankruptcy

of Lehman Brothers in

September 2008. Without the Great Depression, there would have been no

New Deal and no Keynesian revolution in economics. Roosevelt might never

have progressed beyond the New York governor’s mansion in Albany.

Hitler, whose political star was on the wane by the late 1920s, would

have been a historical footnote .

Similarly, without the long-lingering effects of the 2008 crash, there would have been no Brexit, Donald Trump would still be a New York City builder and Europe would not be quaking at the possibility of Marine Le Pen replacing François Hollande as French president.

Not since the 1930s have there been such acute fears of a populist

backlash against the prevailing orthodoxy. As then, a prolonged period

of poor economic performance has led to a political reaction that looks

like feeding back into a desire for a different economic approach. The

early 30s share with the mid-2010s a sense that the political

establishment has lost the confidence of large numbers of voters, who

have rejected “business as usual” and backed politicians they see as

challenging the status quo.

Depression to Dust Bowl: a large cloud appears behind a

truck travelling on Highway 59 in Colorado, May 1936. Photograph:

PhotoQuest/Getty Images

Trump is not the first president to urge an America-first policy: Roosevelt was of a similar mind after he replaced Herbert Hoover

in 1933. Nor is this the first time there has been such a wide gulf

between Wall Street and the rest of the country. The loathing of the

bankers in the 20s hardened into a desire for retribution in the 30s.

According to Lord Robert Skidelsky, biographer of John Maynard Keynes:

“We got into the Great Depression for the same reason as in 2008: there

was a great pile of debt, there was gambling on margin on the stock

market, there was over-inflation of assets, and interest rates were too

high to support a full employment level of investment.”

There are other similarities. The 20s had been good for owners of

assets but not for workers. There had been a sharp increase in

unemployment at the start of the decade and labour markets had not fully

recovered by the time an even bigger slump began in 1929. But while

employees saw their slice of the economic cake get smaller, for the rich

and powerful, the Roaring Twenties were the best of times. In the US,

the halving of the top rate of income tax to 32% meant more money for

speculation in the stock and property markets. Share prices rose sixfold

on Wall Street in the decade leading up to the Wall Street Crash.

Inequality was high and rising, and demand only maintained through a

credit bubble. Unemployment between 1921 and 1929 averaged 8% in the US,

9% in Germany and 12% in Britain. Labour markets had never really

recovered from a severe recession at the start of the 20s designed to

stamp out a post-war inflationary boom.

Above all, in both periods global politics were in flux. From around

1890, the balance of power between the great European nations that had

kept the peace for three quarters of a century after the battle of

Waterloo in 1815 started to break down. The Ottoman and Austro-Hungarian

empires were in decline before the first world war; the US, Germany and

Russia were on the rise.

Brooklyn Daily Eagle front page on Black Thursday. Photograph: Icon Communications/Getty

More importantly, Britain, which had been the linchpin of late

19th-century globalisation had been weakened by the first world war and

was no longer able to provide the leadership role. America was not yet

ready to take up the mantle.

Stephen King, senior economic adviser to HSBC and author of a forthcoming book on the crisis of globalisation, Grave New World,

says: “There are similarities between now and the 1920 and 1930s in the

sense that you had a declining superpower. Britain was declining then

and the US is potentially declining now.”

King

says that in the 20s, the idea of a world ruled by empires was

crumbling. Eventually, the US did take on Britain’s role as the defender

of western values, but not until the 40s, when it was pivotal in both

defeating totalitarianism and in creating the economic and political

institutions – the United Nations, the International Monetary Fund, the

World Bank – that were designed to ensure the calamitous events of the

30s never happened again.

“There are severe doubts about whether the US is able or willing to

play the role it played in the second half of the 20th century, and

that’s worrisome because if the US is not playing it, who does? If

nobody is prepared to play that role, the question is whether we are

moving towards a more chaotic era.”

Deflationary disaster

There are, of course, differences as well as similarities between the

two epochs. At this year’s meeting of the World Economic Forum in

Davos, Switzerland, held in the week of Trump’s inauguration, members of

the global business elite found reasons to be cheerful.

Some took comfort from technology: the idea that Facebook,

Snapchat and Google have shrunk the world. Others said slapping tariffs

on imported goods in an era of complex international supply chains would

push up the cost of exports and make it unthinkable even for a country

as big as the US to adopt a go-it-alone economic strategy. Roberto

Azevêdo, managing director of the World Trade Organisation said: “The

big difference between the financial crisis of 2008 and the early 1930s

is that today we have multilateral trade rules, and in the 30s we

didn’t.”

The biggest difference between the two crises, however, is that in

the early 1930s blunders by central banks and finance ministries made

matters a lot worse than they need have been. Not all stock market

crashes morph into slumps, and one was avoided – just about – in the

period after the collapse of Lehman Brothers.

A ‘Hooverville’ collection of unemployed people’s shack dwellings in Seattle, Washington, in 1933. Photograph: AP

Early signs from data for industrial production and world trade in

late 2008 showed declines akin to those during the first months of the

Great Depression. Policymakers have been rightly castigated for being

asleep at the wheel while the sub-prime mortgage crisis was gestating,

but knowing some economic history helped when Lehman Brothers went bust.

In the early 30s, central banks waited too long to cut interest rates

and allowed deflation to set in. There was a policy of malign neglect

towards the banks, which were allowed to go bust in droves. Faced with

higher budget deficits caused by higher unemployment and slower growth,

finance ministers made matters worse by raising taxes and cutting

spending.

The response to the Crash, according to Adam Tooze in his book The Deluge,

was deflationary policies were pursued everywhere. “The question that

critics have asked ever since is why the world was so eager to commit to

this collective austerity. If Keynesian and monetarist economists can

agree on one thing, it is the disastrous consequences of this

deflationary consensus.”

At the heart of this consensus was the gold standard, the strongly

held belief that it should be possible to exchange pounds, dollars,

marks or francs for gold at a fixed exchange rate. The system had its

own automatic regulatory process: if a country lived beyond its means

and ran a current account surplus, gold would flow out and would only

return once policy had been tightened to reduce imports.

After

concerted efforts by the Bank of England and the Treasury, Britain

returned to the gold standard in 1925 at its pre-war parity of $4.86.

This involved a rise in the exchange rate that made life more difficult

for exporters.

What the policymakers failed to realise was that the world had moved

on since the pre-1914 era. Despite being on the winning side, Britain’s

economy was much weaker. Germany’s economy had also suffered between

1914 and 1918, and was further hobbled by reparations. America, by

contrast, was in a much stronger position.

This changing balance of power meant that restoring the pre-war

regime was a long and painful process, and by the late 20s the strains

of attempting to do so were starting to become unbearable in just the

same way as the strains on the euro – the closest modern equivalent to

the gold standard – have become evident since 2008.

Instead of easing off, policymakers in the early stages of the Great

Depression thought the answer was to redouble their efforts. Peter

Temin, an economic historian, compares central banks and finance

ministries to the 18th-century doctors who treated Mozart with mercury:

“Not only were they singularly ineffective in curing the economic

disease; they also killed the patient.”

Skidelsky explains that in Britain, the so-called “automatic stabilisers”

kicked in during the early stages of the crisis. Tax revenues fell

because growth was weaker while spending on unemployment benefits rose.

The public finances fell into the red.

Supporters of the New Deal agency march through New York

in protest at corporate layoffs, January 1937. Photograph: New York

Times Co/Getty Images

Instead of welcoming the extra borrowing as a cushion against a

deeper recession, the authorities took steps to balance the budget. Ramsay MacDonald’s

government set up the May committee to see what could be done about the

deficit. Given the membership, heavily weighted in favour of

businessmen, the outcome was never in doubt: sterling was under pressure

and in order to maintain Britain’s gold standard parity, the May

committee recommended cuts of £97m from the state’s £885m budget.

Unemployment pay was to be cut by 30% in order to balance the budget

within a year.

The

severity of the cuts split the Labour government and prompted the

formation of a national government led by MacDonald. Philip Snowden, the

chancellor, said the alternative to the status quo was “the Deluge”.

Financial editors were invited to the Treasury to be briefed on measures

being taken to protect the pound, and when one asked whether Britain

should or could stay on the gold standard, the Treasury mandarin Sir

Warren Hastings rose to his feet and thundered: “To suggest we should

leave the gold standard is an affront not only to the national honour,

but to the personal honour of every man or woman in the country.”

The show of fiscal masochism failed to prevent fresh selling of the

pound, and eventually the pressure became unbearable. In September 1931,

Britain provided as big a shock to the rest of the world as it did on 23 June 2016, by coming off the gold standard.

The pound fell and the boost to UK exports was reinforced six months

later when the coalition government announced a policy of imperial

preference, the erection of tariff barriers around colonies and former

colonies such as Australia and New Zealand.

Britain was not the first country to resort to protectionism. The now infamous Smoot-Hawley tariff had

been announced in the US in 1930. But America had a recent history of

protectionism – it had built up its manufacturing strength behind a 40%

tariff in the second half of the 19th century. Britain, as Tooze

explains, had been in favour of free trade since the repeal of the corn laws in 1846.

“Now it was responsible for initiating the death spiral of

protectionism and beggar-thy-neighbour currency wars that would tear the

global economy apart.”

An elderly woman sits by a shop window full of adverts

for cigarettes, 1935. Photograph: General Photographic Agency/Getty

Images

Britain’s 1931 exit from the gold standard meant it secured

first-mover advantage over its main rivals. For Germany, the pain was

especially severe, since the country’s mountain of foreign debt ruled

out devaluation and left Chancellor Brüning’s government with the choice

between default and deflation. Brüning settled for another round of

austerity, not realising that for voters there was a third choice: a

party that insisted that national solutions were the answer to a broken

international system.

The reason borrowing costs were slashed in 2008 is that central bankers knew their history. Ben Bernanke,

then chairman of America’s Federal Reserve, was a student of the Great

Depression and fully acknowledged that his institution could not afford

to make the same mistake twice. Interest rates were cut to barely above

zero; money was created through the process known as quantitative

easing; the banks were bailed out; Barack Obama pushed a fiscal stimulus

programme through Congress.

But the policy was only a partial success. Low interest rates and

quantitative easing have averted Great Depression 2.0 by flooding

economies with cheap money. This has driven up the prices of assets –

shares, bonds and houses – to the benefit of those who are rich or

comfortably off.

For those not doing so well, it has been a different story. Wage

increases have been hard to come by, and the strong desire of

governments to reduce budget deficits has resulted in unpopular

austerity measures. Not all the lessons of the 1930s

have been well learned , and the over-hasty tightening of fiscal policy

has slowed growth and caused political alienation among those who feel

they are being punished for a crisis they did not create, while the real

villains get away scot-free . A familiar refrain in both the referendum

on Brexit and the 2016 US presidential election was: there might be a

recovery going on, but it’s not happening around here.

Authoritarian solutions

Internationalism died in the early 30s because it came to be

associated with discredited policies: rampant speculation, mass

unemployment, permanent austerity and falling living standards.

Totalitarian states promoted themselves as alternatives to failed and

decrepit liberal democracies. Hitler’s Germany was one, Stalin’s Soviet

Union another. While the first era of globalisation was breaking up,

Moscow was pushing ahead with the collectivisation of agriculture and

rapid industrialisation.

What’s more, the economic record of the totalitarian countries in the

30s was far superior to that of the liberal democracies. Growth

averaged 0.3% a year in Britain, the US and France, compared with 3.1% a

year in Germany, Italy, Japan and the Soviet Union.

Erik Britton, founder of the consultancy Fathom , says: “The 1920s

saw the failure of liberal free-trade, free-market policies to deliver

stability and growth. Alternative people came along with a populist

stance that really worked, for a while.”

There is, Britton says, a reason mainstream parties are currently

being rejected: “It is not safe to assume you can deliver unsatisfactory

economic outcomes for a decade without a political reaction that feeds

back into the economics.”

A car goes on sale for $100 after the Wall Street Crash. Photograph: PPP

Economic devastation caused by the Great Depression did eventually

force western democracies into rethinking policy. The key period was the

18 months between Britain coming off the gold standard in September

1931 and Roosevelt’s arrival in the White House in March 1933.

Under Hoover, US economic policy had been relentlessly deflationary.

As in Germany – the other country to suffer most grievously from the

Depression – there was a dogged insistence on protecting the currency

and on balancing the budget.

That changed under FDR. Policy became both more interventionist and

more isolationist. If London could adopt a Britain-first policy, then so

could Washington. Roosevelt swiftly took the dollar off the gold

standard and scuppered attempts to prevent currency wars. Wall Street

was reined in; fiscal policy was loosened. But it was too late. By then,

Hitler was chancellor and tightening his grip on power. Ultimately, the

Depression was brought to an end not by the New Deal, but by war.

King says the world is already starting to become more protectionist

in terms of movement of capital and labour. Trump has been naming and

shaming US companies seeking to take advantage of cheaper labour in the

emerging countries, while Brexit is an example of the idea that

migration needs to be controlled.

The US supported the post-war global instutional framework: the UN, IMF and European Union, through the Marshall plan.

“It tried to create a framework in which individual countries could

flourish,” King adds. “But I don’t see that [happening again] in the

future, which creates difficulties for the rest of the world.”

Campaign posters for Britain’s national government

coalition spanning two elections. Photograph: Conservative Party

Archive/Getty Images

So far, financial markets have taken a positive view of Trump. They

have concentrated on the growth potential of his plans for tax cuts and

higher infrastructure spending, rather than his threat to build a wall

along the Rio Grande and to slap tariffs on Mexican and Chinese imports.

There is, though, a darker vision of the future, where every country

tries to do what Trump is doing. In this scenario, a shrinking global

economy leads to shrinking global trade, and deflation means personal

debts become more onerous. “It becomes a vicious, self-fulfilling

cycle,” Britton says. “People seek answers and find it in

authoritarianism, populism and protectionism. If one country can show it

works, there is a strong temptation for others to follow suit.”

This may prove too pessimistic. The global economy is growing by

around 3% a year; Britain and the US (if not the eurozone) have seen

unemployment halve since the 2008-09 crisis; low oil prices have kept

inflation low and led to rising living standards.

Even so, it is not hard to see why support for the policy ideas that have driven the second era of globalisation

– free movement of capital, goods and people – has started to fracture.

The winners from the liberal economic system that emerged at the end of

the cold war have, like their forebears in the 20s, failed to look out

for the losers. A rising tide has not lifted all boats, and those who do

not consider themselves the beneficiaries of globalisation have grown

weary of hearing how marvellous it is.

The 30s are proof that nothing in economics is inevitable. There was

eventually a backlash against the economic orthodoxies and Skidelsky can

see why there is another backlash happening today. “Globalisation

enables capital to escape national and union control. I am much more

sympathetic since the start of the crisis to the Marxist way of

analysing things.

“Trump will be impeached, assassinated or frustrated by Congress,”

Skidelsky suggests. “Or he will remain popular enough to overcome the

liberal consensus that he is a shit of the first order. After all, a lot

of people agree with what he is doing.”

No comments:

Post a Comment